Arranging building insurance is only half the equation. The level of cover you choose is just as important, and that starts with understanding your property's Reinstatement Cost. Many property owners assume their insurance should reflect the property's market value. In reality, insurers are interested in something entirely different-the amount it would cost to rebuild the property if it were completely destroyed.

Knowing what reinstatement cost is, how it is calculated, and when a professional assessment is worthwhile can help you avoid both underinsurance and unnecessarily high premiums.

Before looking at the calculation, it's important to define reinstatement cost. Reinstatement Cost is the total amount required to rebuild a property to the same standard it was before it was damaged or destroyed. It reflects the cost of reconstruction rather than the property's sale price or market value.

A reinstatement assessment focuses on the cost of replacing the physical building, taking into account current construction prices, professional services, demolition, and compliance with current building regulations.

The two figures are rarely the same.

Your insurance policy is based on the declared Building replacement cost. If that figure is too low, the insurance payout may not fully cover rebuilding costs after a major loss. If it is too high, you could end up paying higher premiums without receiving any additional benefit.

Construction costs across Australia continue to fluctuate due to changes in labour availability, material pricing, and regulatory requirements. A rebuilding estimate prepared several years ago may no longer reflect today's costs.

For that reason, reviewing your reinstatement value periodically is an important part of managing your property's insurance.

One of the most common questions property owners ask is, "How is reinstatement cost calculated?" There isn't a single fixed formula because every property is different. Instead, the assessment considers a range of construction-related factors to estimate the total rebuilding cost.

Together, these factors provide a realistic estimate of what it would cost to reconstruct the property to its existing standard.

For many standard residential properties, insurer-provided rebuilding calculators can provide a useful preliminary indication of the potential cost to rebuild a property.

Industry-recognised tools and similar rebuilding calculators used within the Australian insurance sector estimate rebuilding costs based on property-specific information and construction cost data.

The resulting estimate can assist property owners, insurers and advisers in establishing an initial indication of an appropriate level of insurance cover for standard residential properties.

However, these calculators provide an indicative estimate only and should not be regarded as a substitute for a detailed Reinstatement Cost Assessment prepared by a Qualified Quantity Surveyor. Automated calculators may not capture the full extent of site-specific, construction, regulatory and market considerations associated with an individual property, including demolition and debris removal, professional fees, escalation, specialist construction requirements, heritage considerations, difficult site conditions and other project-specific factors.

For complex, high-value or non-standard properties, a professionally prepared Reinstatement Cost Estimate provides a more robust and defensible assessment of the likely cost to reinstate the property following a major loss event.

Rebuilding doesn't begin with construction. If a building is severely damaged, the existing structure often needs to be demolished and removed before rebuilding can commence.

Depending on the size and location of the property, demolition costs can represent a significant part of the overall reinstatement value. Ignoring these expenses can result in insufficient insurance cover.

Another commonly overlooked area is professional services. A complete rebuilding project often requires input from various consultants before construction can begin.

These expenses form part of the overall rebuilding process and should generally be considered when determining an accurate reinstatement value.

Even if your insurance was adequate a few years ago, today's rebuilding costs may be very different.

These factors can significantly influence rebuilding costs over time. Reviewing your insurance cover regularly helps ensure your policy reflects current market conditions rather than outdated construction rates.

Online calculators are useful for many standard homes, but they have limitations.

In these situations, engaging a suitably qualified Quantity Surveyor who is a full voting member of the AIQS or RICS and holds the professional designation of Chartered or Certified Quantity Surveyor provides greater assurance that the assessment is undertaken by an appropriately experienced and recognised professional.

A professionally prepared Insurance Valuation Report provides an independent assessment of a property's rebuilding cost.

Rather than relying on general estimates, the report evaluates the individual building and considers the factors that influence reconstruction costs.

The report provides insurers and property owners with a reliable basis for determining appropriate building insurance cover.

Calculating reinstatement value requires more than estimating construction costs. Quantity Surveyors specialise in measuring and assessing building costs using recognised industry methodologies and current market data.

At Quantum QS, our experienced team prepares independent insurance valuations and reinstatement cost assessments for residential, commercial, strata, and specialised properties throughout Australia. Our assessments are based on current construction pricing, property-specific analysis, and established cost planning principles, helping property owners make informed insurance decisions with greater confidence.

Understanding what reinstatement cost is is an important step in ensuring your property is insured for the amount it would actually cost to rebuild. While online calculators can provide a useful guide for many homes, larger or more complex properties often benefit from a professionally prepared Insurance Valuation Report that considers the full scope of rebuilding costs.

If you're reviewing your insurance cover or require an independent assessment of your property's Building replacement cost, Quantum QS can provide accurate reinstatement cost assessments tailored to your property's construction, location, and current market conditions.

What is reinstatement cost?

Reinstatement Cost is the estimated amount required to rebuild a property to its previous condition after a total loss. It reflects rebuilding costs rather than market value.

Is reinstatement cost the same as market value?

No. Market value includes factors such as land value and property demand, while reinstatement cost focuses solely on rebuilding the structure.

How is reinstatement cost calculated?

It is calculated by considering construction costs, demolition, professional fees, building materials, labour, permits, and other expenses associated with rebuilding the property.

What is included in an Insurance Valuation Report?

An Insurance Valuation Report generally includes an assessment of the building, current construction rates, demolition costs, professional fees, and the estimated rebuilding cost required for insurance purposes.

When should I obtain a professional reinstatement cost assessment?

A professional assessment is recommended for commercial properties, strata buildings, heritage homes, architect-designed residences, and any property where standard online calculators may not accurately reflect rebuilding costs.

Jul 9, 2026

The level of cover you choose is just as important, and that starts with understanding your property's Reinstatement Cost

Jul 8, 2026

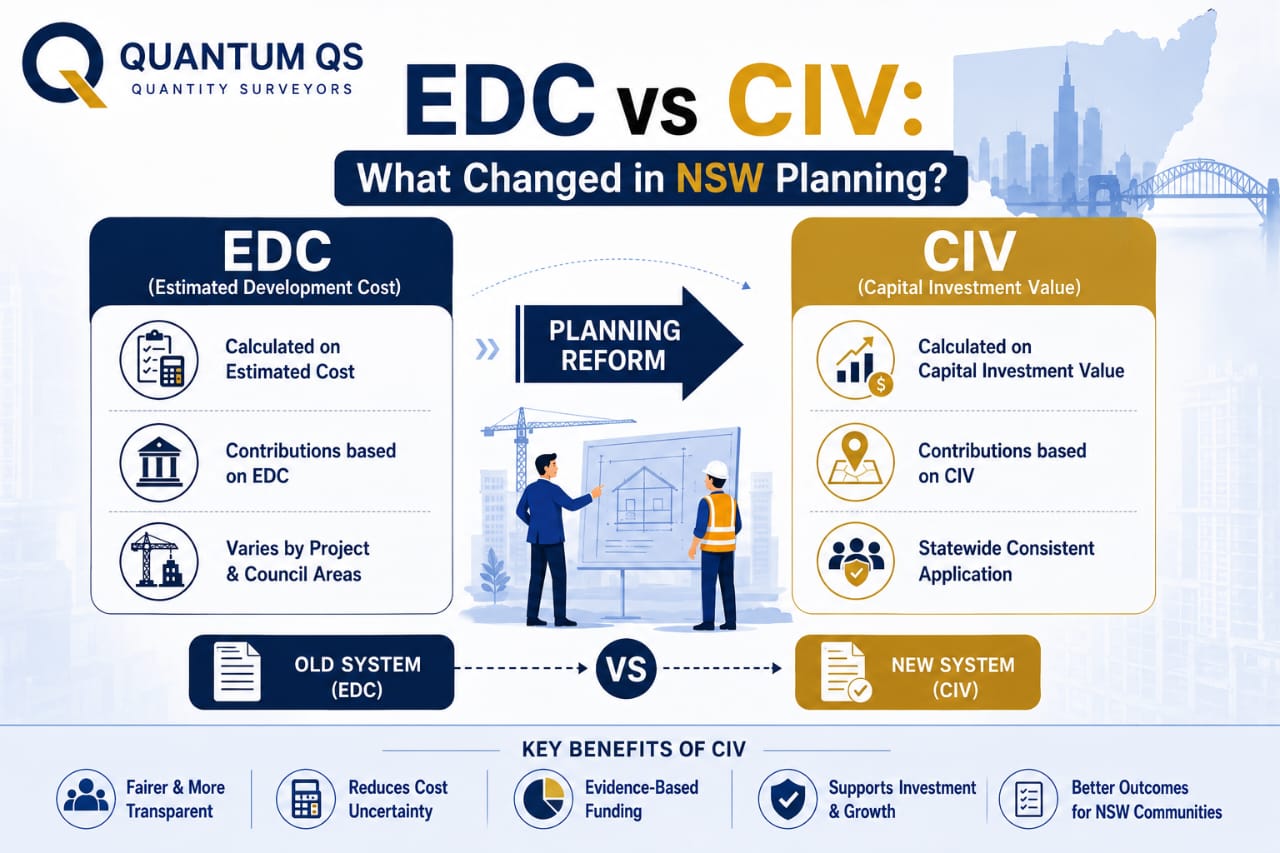

For many years, developers, property owners, consultants, and councils across New South Wales relied on Capital Investment Value (CIV)

Jul 7, 2026

When preparing a Development Application (DA) in New South Wales, one of the documents you may be asked to provide is an EDC Report.