Most property owners assume their insurance is "sorted" once the policy is in place. The reality is, the effectiveness of that cover depends entirely on whether the insured value actually reflects what it would cost to rebuild the property today.

That's where a property insurance valuation comes in. It's not about what the property is worth on the market, and it's not based on what you paid for it. It's about one thing - what it would cost to rebuild it properly if something went wrong.

With construction costs in Australia shifting constantly, relying on old figures or rough estimates can quietly create a serious financial gap.

A property insurance valuation is essentially a detailed calculation of your property's rebuilding cost.

It takes into account:

It doesn't include land value, and it's not influenced by market demand. The focus is strictly on the property replacement value - what it takes to physically reconstruct the building.

A lot of people only realise the importance of an accurate valuation when they need to make a claim. By then, it's too late to fix.

One of the biggest risks is underinsurance.

If your building insurance valuation is too low, your insurer may not cover the full cost of rebuilding. That shortfall doesn't disappear - you cover it yourself.

And with construction costs rising, even a small underestimation can turn into a significant financial hit.

An accurate building valuation helps avoid that situation altogether.

If you're involved in a strata property, this isn't just a "good idea" - it's often a requirement.

Owners Corporations are generally expected to:

Missing this step doesn't just create risk - it can also lead to legal and financial consequences. Learn more about how we support strata schemes through our strata management services.

On the other side, over-insuring a property is a quieter problem, but still a real one.

If the property replacement value is overstated:

A proper insurance valuation in Australia keeps things balanced. You're covered properly, without overpaying.

This is where a lot of confusion comes in.

Market value is what someone is willing to pay for the property. It includes land value, location, and demand.

Replacement value is different. It's purely about construction - what it costs to build the same structure again.

Insurance should always be based on property replacement value, not market value.

A valuation isn't something you do once and forget about.

You should look at updating your valuation of property insurance if:

Keeping it updated is what keeps your insurance relevant.

It's tempting to rely on estimates or online calculators, but they rarely capture the full picture.

A proper valuation involves:

That level of detail is what makes a building insurance valuation dependable.

When something does go wrong, your valuation becomes a key reference point.

If it's accurate, the claims process tends to be smoother. There's less room for dispute, and the insurer has a clear benchmark to work from.

If it's not accurate, things can get complicated - delays, disagreements, or reduced payouts.

That's where having proper insurance claim support backed by a solid valuation really matters.

A few patterns show up again and again:

None of these reflect actual rebuilding costs.

Have questions about the valuation process or what's covered? Visit our frequently asked questions page for more detail.

Getting your insurance valuation right isn't just about ticking a box.

It's about:

It's one of those things that doesn't feel urgent - until it suddenly is.

Quantum QS approaches insurance valuation in Australia from a construction and cost perspective, not just a theoretical one.

That means the focus stays on real rebuilding costs, current market conditions, and compliance requirements - so the numbers actually hold up when they're needed.

An accurate property insurance valuation is one of those things that quietly protects you in the background - until the moment it becomes critical.

With construction costs constantly changing, relying on outdated figures can leave a gap you don't want to deal with later.

Getting the property replacement value right isn't complicated, but it does require attention. And for property owners, that attention can make a significant difference when it matters most.

Contact Quantum QS today to get an accurate, professionally prepared insurance valuation for your property.

Frequently Asked Questions

What is a property insurance valuation?

It’s a calculation of how much it would cost to rebuild your property, used to set the right level of insurance coverage.

How often should it be updated?

Every 2–3 years is a good rule of thumb, or sooner if there are major changes.

Is a building insurance valuation required for strata properties?

In many cases, yes. Strata regulations often require regular independent valuations.

What does property replacement value include?

It includes construction costs, labour, professional fees, demolition, and compliance requirements - but not land value.

Why is an accurate building valuation important for claims?

Because it provides a clear benchmark, helping support claims and reduce disputes.

Jul 9, 2026

The level of cover you choose is just as important, and that starts with understanding your property's Reinstatement Cost

Jul 8, 2026

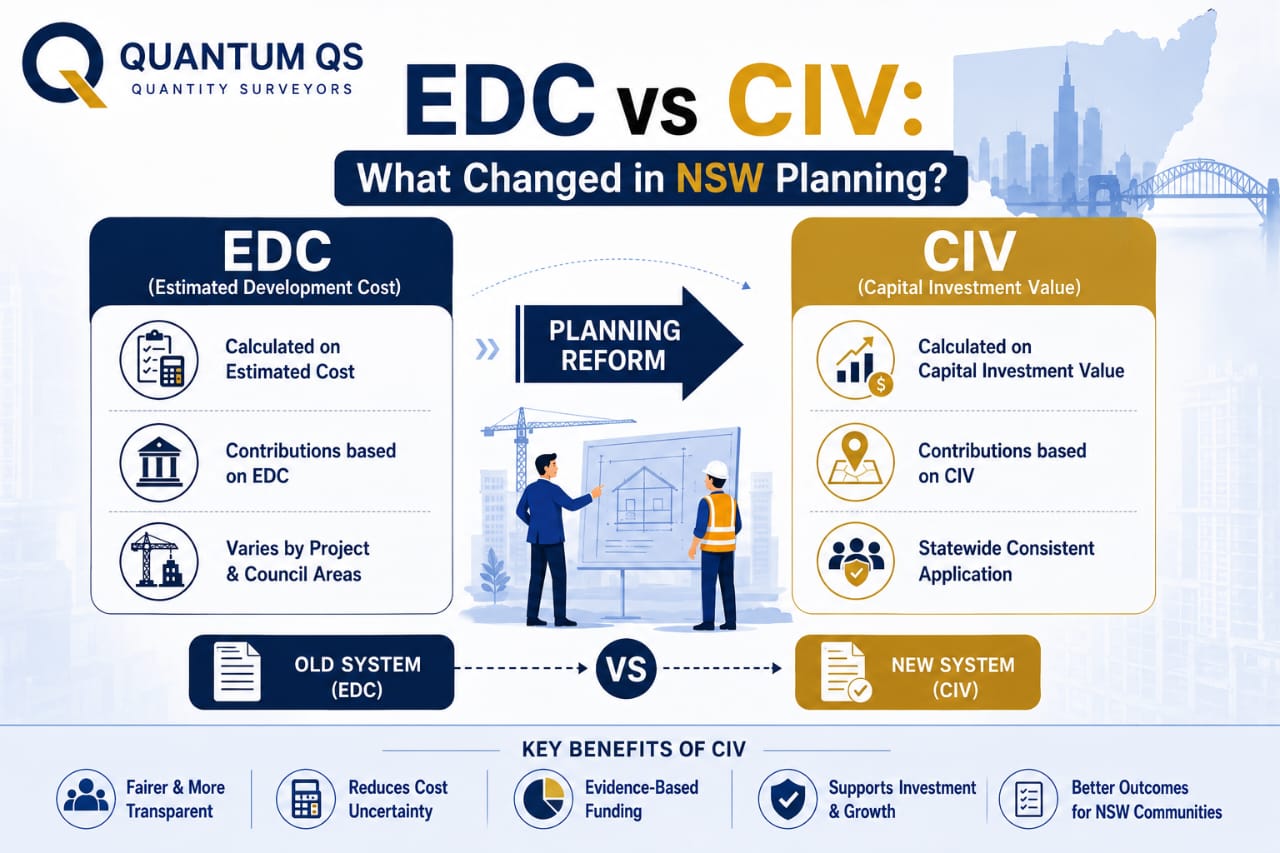

For many years, developers, property owners, consultants, and councils across New South Wales relied on Capital Investment Value (CIV)

Jul 7, 2026

When preparing a Development Application (DA) in New South Wales, one of the documents you may be asked to provide is an EDC Report.